P&C insurance carriers around the globe are impacted by COVID-19. This is our initial view on how operations and IT need to respond to the "New Normal”.

Context

The COVID-19 pandemic, with millions infected, is having an unprecedented impact across the globe with completely unforeseen economic effects.

The near-term economic impact is significant, and the recovery is predicted to be very lumpy, as the world economy re-opens. Most businesses, large and small, have been forced to either completely suspend operations, or adopt a highly restricted operating model that results in sharply reduced revenue. Among the biggest winners so far are companies with digital products that can be purchased and serviced completely or mostly via the internet. This is very likely to be the case for insurance, a product that is ideally suited for a completely digital operating model.

Property and casualty carriers, especially those with inflexible back office operations and technology, are in the extremely difficult situation of attempting to respond quickly and iteratively to continuously evolving demands, whilst attempting to rapidly implement cost efficiencies and digital capabilities for interacting with prospects, policyholders, brokers, agents, and service partners.

Business Impact

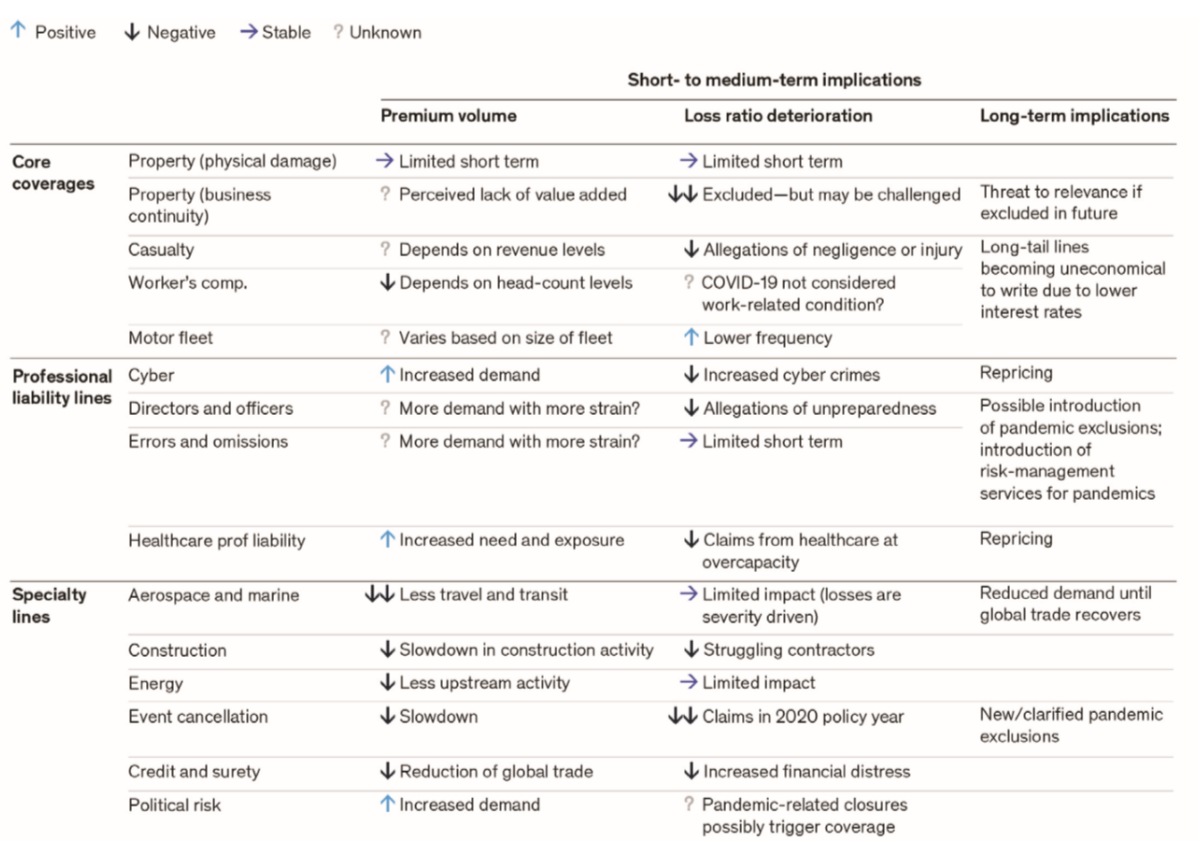

The overall business impact of COVID-19 on the P&C industry varies considerably across lines of business and geographies. In some lines of business, demand and premium volume is actually increasing, while claim submissions and premium is decreasing in others. We have reviewed a number of reports by various analyst firms and concluded that the following extract from McKinsey & Company’s “Coronavirus Response: Short- and long-term actions for P&C insurers” provides a concise and comprehensive view of likely business impact across the globe.

*Source: McKinsey & Company “Coronavirus Response: Short- and long term actions for P&C insurers

Impact on P&C Commercial Lines

The main takeaways from an operational and IT perspective based on the McKinsey report and similar analyses we’ve reviewed are as follows:

- The impact varies significantly by geography and line of business. There is no “one size fits all” response.

- Flexibility and agility will be critical. Unfortunately, many traditional P&C carriers, especially in the commercial/specialty space are ill-equipped to move quickly.

- As mentioned, specific lines of business will be impacted to varying degrees. Some of the more significant examples we see affecting our P&C customers include:

- Employers Liability - projected to experience a sharp reduction in premium volume resulting from severe, near term business contraction and very high unemployment. Some carriers are likely to exit this line or dramatically restrict their risk appetite.

- Motor and Commercial Motor – COVID-19 has resulted in a dramatic reduction in exposure units (revenue miles driven), claim submission frequency and lowered renewal/retention ratios. Waze reports 60% drop in miles driven globally during pandemic1. In response, a few nimble, aggressive carriers are offering rebates and discounts at renewal, in order to retain market share, which is likely to leave less agile competitors with a reduced market share.

- Cyber Security – an uptick in demand in the near term is a growth opportunity for carriers who are sufficiently prepared operationally and with supporting technology.

While most carrier’s financial health remains quite strong, for now, some have begun reporting Q1 2020 financial losses and set aside “provisional reserves” for anticipated COVID-19 liabilities and are bracing for difficult and unpredictable financial challenges in Q2 and Q3 and beyond. On the other hand, one of our mid-sized specialty carriers recently told us that “Q1 was slightly ahead of plan on premiums and slightly better on loss ratios, so it was our best quarter in years.”

There are going to be winners and losers in the coming months. While some carriers are pulling back into a bunker mentality, others are looking for opportunities. CIOs are likely to be caught in the middle of competing priorities as different lines of business need to move quickly in very different directions.

Operations Impact

Mindtree currently supports over 50 insurance companies of varying sizes across multiple lines of business around the globe. We reached out to our customers and account teams to assess the current situation. Among the trends we are seeing:

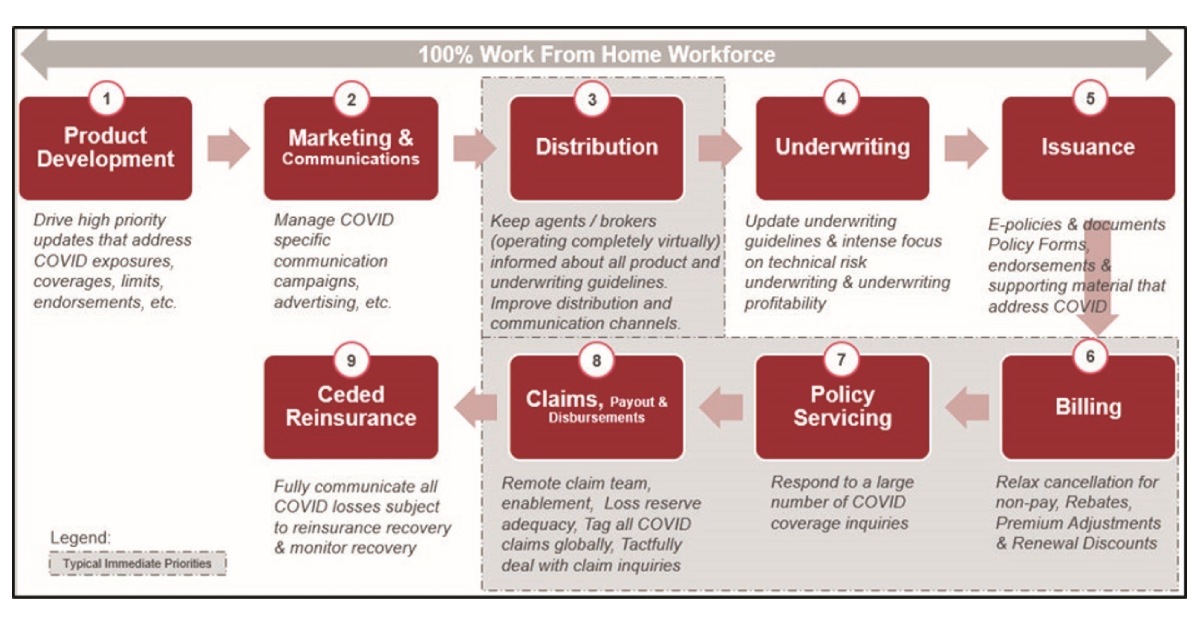

- Call centres and service desks - receiving very high call volumes from concerned policyholders, agents/brokers, and claimants with inquiries about coverages, billing, and related topics whilst the carrier workforce is operating 100% virtually. This poses serious customer service challenges for small to mid-sized carriers that lack robust virtual call centre capabilities, productivity tools, and automation to scale and reduce the load on over-stretched operations staff. A related problem is the challenge of onboarding new staff in a work from home operating model.

- COVID-19 has triggered a heightened imperative for carriers to become more digital across the entire insurance operations lifecycle, with an initial priority focus on producer management, billing, Policy Servicing and claims functions to make them more responsive and cost effective. One of our UK commercial lines carriers decided to roll out additional claims self-service capabilities on an emergency basis using a minimum viable product approach.

- Many clients plan for a limited return to the traditional workplace model for the remainder of 2020. As a result, any stop-gap measures introduced to quickly enable a work from home workforce, need to be significantly enhanced to address employee productivity and communication. It is also critical to improve overall network security and related risks that arise from a work from home operating model.

- Several clients are re-evaluating their “on prem” data centre operations and placing greater urgency on shifting where possible in the near term to a more cloud-enabled, usage based variable cost model.

Core Operations - Demand for changes and immediate priorities

Looking holistically across P&C core operations, we see a number of opportunities and challenges facing CIOs in the coming weeks and months.

Hotspots for immediate action include:

- Distribution

- In-force servicing

- Billing

- Claims

We are also seeing high priority ad hoc requests in the Data/Analytics arena in addition to the operating impacts mentioned above. Carriers that do not have flexible data extraction, reporting and analytics environments will struggle. Examples include:

- Ad hoc analysis of various core transaction data including premium/sales data, claims and loss reserves and related metrics.

- Forward-looking estimation models that provide the senior executive leadership team with the projected impact of COVID-19 on the carrier’s financial performance, based on the latest available data, various scenarios and assumptions.

Technology initiatives to address the impact

CIOs and CTOs are being called upon to quickly re-prioritise and deploy resources to address COVID-19-related initiatives and to prioritise them to “Act Now” based on their specific situation.

While it is not feasible in this whitepaper to cover all the potential IT responses to business and operational challenges, a few themes clearly stand out.

Near Term (0-3 months)

CIOs need to be prepared for continuously shifting priorities and have solution approaches lined up in the following areas:

- Digital Quick Hit Capabilities - Most carriers have the rudimentary infrastructure to enable self-service capabilities for policyholders and agents/brokers. Many are looking to leverage this and take incremental steps forward:

- Simple read-access to key information such as quotes, policy documents, claims status, endorsement requests, etc.

- Improve policyholder experience where practical.

- Claim triaging and automated routing to the most appropriate claim case manager and adjuster

- Streamlined premium waivers, policy reinstatements for inadvertent cancellations

- Standalone “microsites” that provide stakeholders with critical updates, FAQs, etc.

- Remote Work Force Continuity & Infrastructure - Whether it is productivity and collaboration tools like Microsoft Teams, Slack or mission critical data centre operations hardening, the current remote workforce situation brings new risks and challenges. CIOs need a go-forward plan to address these issues with a focus on selectively engaging cloud solutions and platforms to enhance scalability, continuity and security.

- Dev Ops/IT Operations/Core Processing

- Selectively apply product platform “hot fixes” that reduce process bottlenecks, enable operational streamlining or expose capabilities for web self-service.

- Virtual Pods - Enable teams collaborating remotely to provide critical patches and product changes quickly and effectively in an agile manner.

- Quickly and continually update rating engines to remain competitive in a highly dynamic market.

- Intelligent Automation - Most carriers have implemented RPA solutions, but frequently limited to basic, low-level back office tasks. The current crisis provides a strong incentive to revisit RPA and quickly apply it to more critical processes in billing, claims or policy servicing that can be augmented wholly or in part by the more robust capabilities available in the current crop of RPA/IA tools.

- Campaign Operations – Swift execution of COVID-19 critical communications campaigns and updates to corporate portals, websites and social media with the latest COVID-19 content.

- Data/Cognitive – tagging all COVID-19 claims across the enterprise for aggregate loss reserve and financial liability assessment, IBNR estimating and supporting senior executive needs for COVID-19 impact on statutory and GAAP financials based on various economic assumptions and scenarios.

Medium Term (3-6 months or more)

More challenging situations exist when a diverse set of application systems need to be modified in response to rapidly changing conditions. CIOs need to have a rapid response plan for implementing policy rebates, pricing updates, forms changes and other COVID-19 specific needs into the supporting systems for every insurance product. The ability to execute quickly on these imperatives varies greatly based on the number and the various technologies of the core platforms that are in place. At minimum we believe CIOs need to focus on:

- Digital - Look to service enable end-to-end key areas such as claims to allow for mostly digital claims processing from both external stakeholders (policyholders/claimants) and internal (call centres, claims adjusting and servicing).

- Data/Cognitive - determine if any CAT loss modeling and BI processes can be re-factored to meet COVID-19 senior executive data/reporting needs, identify any ad-hoc, quasi-production data collection processes introduced for COVID-19 and productionise them in order to be more responsive and efficient for providing COVID-19 critical data and financial impact estimation modeling and data presentation.

- Cloud – Analyze the “on-prem” data centre for immediate opportunities to transition to a more flexible, secure and scalable cloud approach and explore opportunities to reduce IT Ops costs and convert from fixed CapEx to variable OpEx based on transaction volume.

- Dev Ops/IT Operations/Core Processing – Insurance Product Management (coverages, limits, rating etc.). Where existing tools fall short, consider quickly “bolting on” a modern product engine for new products that can co-exist with existing platforms, dealing with any limitations on the administration side.

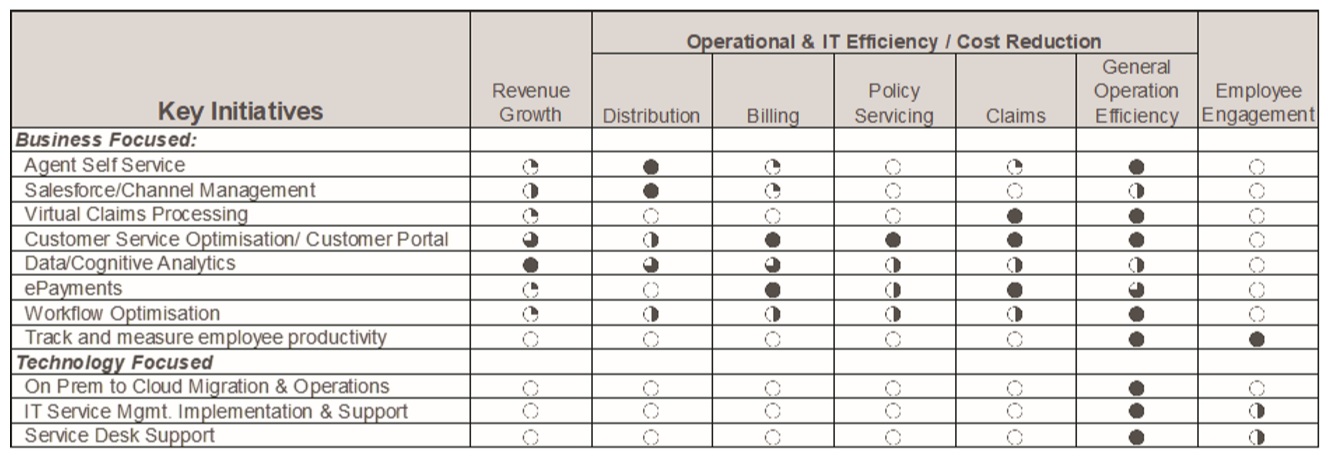

Our insurance clients have initiated the following key initiatives on a high priority basis in response to COVID-19 with the objective to unlock value in the following areas and most are very laser focused on operational, cost efficiencies and cost takeout.

Summary

COVID-19 has impacted the world on a global scale and a great deal of uncertainty still lies ahead. Carriers who take immediate action and develop a plan for the near term to make their operations and IT ecosystems more digital, flexible, nimble, and very cost efficient are very likely to emerge far ahead of their competitors as the world economy comes back online.

Download the whitepaper to learn more